THE COPPER SYSTEM IS BREAKING

AI, Cooling, and the Hidden Constraint No One Is Pricing

The next generation of data centers is not being built like the last.

They are being rebuilt around liquid cooling systems—a structural shift driven by the power density of AI workloads. As compute scales, air cooling fails. Heat becomes the limiting factor. And solving heat requires more than engineering innovation.

It requires materials.

Specifically, it requires copper.

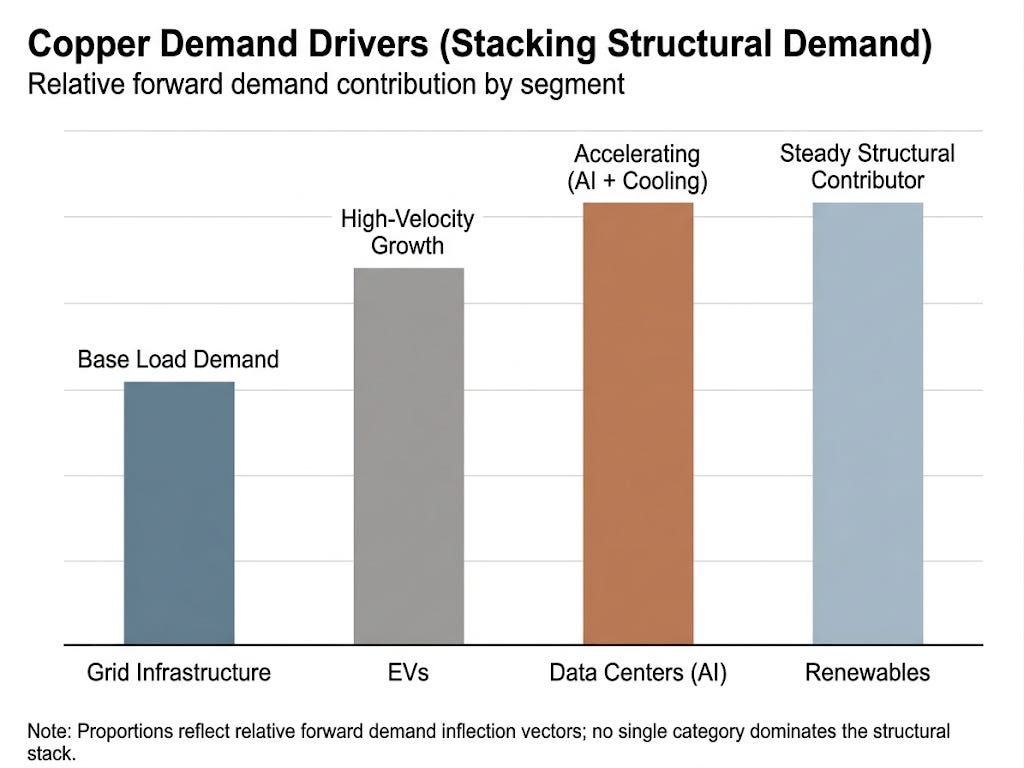

A New Layer of Demand

Copper has always been central to industrial growth—wiring, motors, and grid infrastructure. But AI is introducing a new category of demand layered on top of an already tight system.

Electric vehicles require significantly more copper than internal combustion engines. Grid expansion is accelerating to support electrification. Renewable systems are structurally copper-intensive.

And now, AI data centers are adding incremental demand through both power delivery and liquid cooling systems.

This is not substitution. It is stacking demand.

As Ross Givens, founder of Traders Agency and lead analyst behind its investment research, recently noted, AI infrastructure, EV adoption, and grid expansion are all converging on the same input: copper.

He’s right to frame it this way. What appear to be separate growth narratives are, in reality, a single system drawing from the same constrained resource base—and that is how shortages become structural.

From Mining Problem to System Problem

The prevailing narrative is simple: mining isn’t keeping up.

That’s true—but incomplete.

Copper does not move from ore to infrastructure in a straight line. It moves through a processing chain—one that is increasingly fragile and geopolitically constrained.

China, the world’s largest exporter of sulfuric acid—a critical input in copper and nickel extraction—has begun restricting exports. At the same time, global sulfur markets are tightening, with prices rising and availability becoming less certain.

This matters more than it appears.

Sulfuric acid is not optional. It is foundational to modern metal processing. Without it, the ability to convert ore into usable copper is impaired—regardless of how much material exists in the ground.

The constraint is no longer just geological.

It is chemical.

It is logistical.

And increasingly, it is political.

The Market Is Starting to Adjust

When Amazon Web Services becomes a direct customer of copper produced from a Rio Tinto venture, it signals something important:

End users are no longer passive participants in commodity markets.

They are moving upstream.

Securing supply.

Financing production.

Locking in access.

This is how markets behave when pricing mechanisms begin to fail.

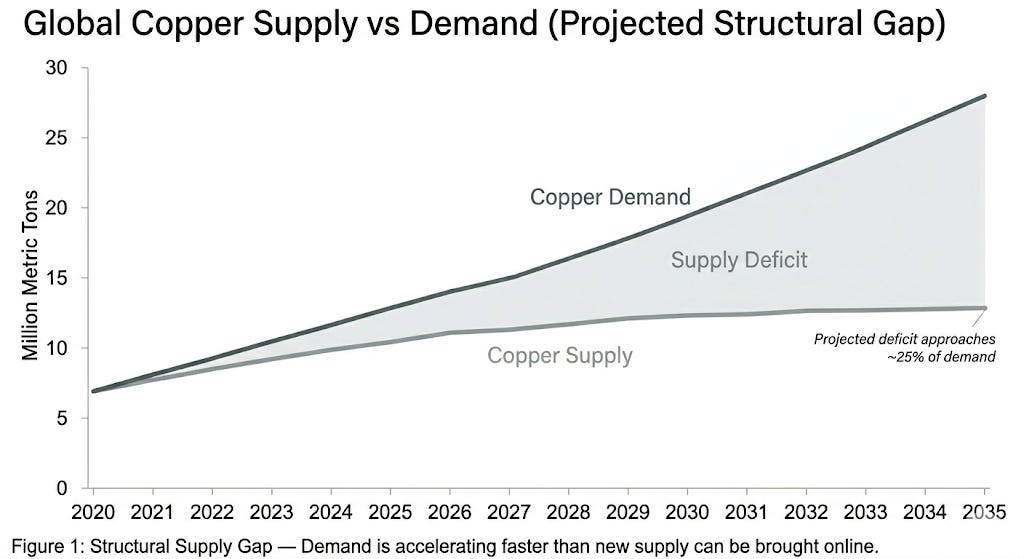

Structural Shortages, Not Cycles

Estimates of future copper deficits—some pointing to shortages approaching 25% of projected demand—are often framed as cyclical imbalances.

They are not.

They are the result of a system under simultaneous pressure:

Demand accelerating across multiple fronts

Processing capacity constrained by inputs and geopolitics

Supply response limited by time, capital, and permitting realities

This is not a gap that closes quickly.

It is a constraint that compounds.

What the Market Is Missing

The focus remains on mining.

But the more important question is where control is shifting.

In constrained systems, value does not accrue evenly. It concentrates at the points where:

conversion happens

validation happens

and access is controlled

Copper is not just becoming more valuable.

It is becoming more strategic.

Closing Thought

The story is not that copper demand is rising.

The story is that the system required to deliver copper—at scale, reliably, and under growing geopolitical tension—is beginning to strain.

And when systems strain, markets don’t adjust smoothly.

They reset around whoever controls access.

— Eric Greene

Founder, Greene Financial Advisory

Founder & Chief Architect, TCE12 Corridor Initiative